For sustainability reporting, 2025 was a turbulent year with a lot of unknowns. How does the sustainability reporting landscape look at the beginning of 2026 and how to navigate this period of change?

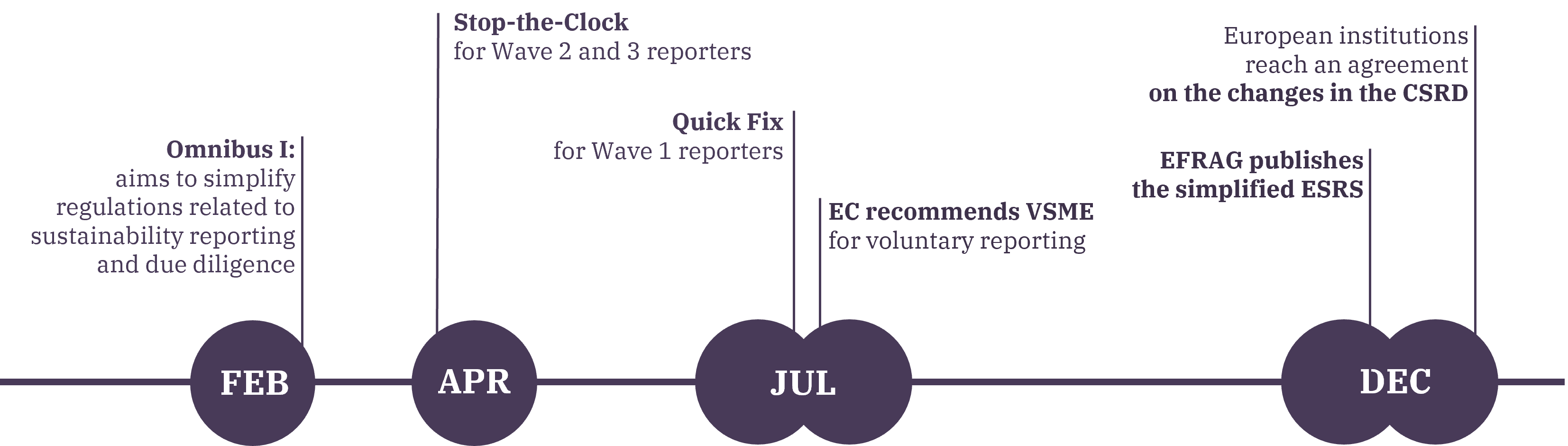

In February 2025, as part of the Omnibus I package, the European Commission decided to narrow the CSRD scope (the number of companies due for mandatory reporting) and simplify the initial ESRS. By mid-year, two, so to speak, interim solutions had been adopted: the start of reporting for Wave 2 and 3 companies was postponed by two years, while Wave 1 reporters were granted several phase-in reliefs regarding the information to be included in the report.

In addition, in July, the European Commission officially recommended the VSME standard for voluntary sustainability reporting. Although the standard’s title retains the reference to small and medium-sized enterprises, the text of the recommendation states that it is intended for “enterprises outside the scope of the CSRD”, i.e. those that exceed the SME definition criteria but will not meet the revised CSRD scope criteria.

In December, EFRAG published and submitted drafts of the simplified ESRS to the European Commission for review. Shortly before the end of the year, the European institutions agreed on the main changes to the CSRD, and the European Parliament voted on the scope of the CSRD.

So which companies shall prepare a sustainability report?

According to the currently applicable regulations, Wave 1 companies (public interest entities with more than 500 employees), which prepared their first ESRS-compliant sustainability statement for 2024, continue to report.

The 2025 Stop-the-Clock amendments to the Law on Sustainability Disclosures postpone the start of sustainability reporting for Wave 2 and 3 companies by two years:

large companies will have to report starting from the FY2027;

listed SMEs will have to report starting from the FY2028.

In addition, the Omnibus I package aims to narrow the scope of the CSRD, namely to reduce the number of companies for which an ESRS-compliant sustainability reporting is mandatory. At the end of 2025, the European institutions negotiated and voted on the following:

the Wave 2 will include only large companies with more than 1,000 employees and a turnover exceeding EUR 450 million;

the Wave 3 companies – listed SMEs – will be excluded from the CSRD scope.

These changes are still subject to approval by the European Council, followed by publication of the amending directive in the EU Official Journal and transposition at national level. The Council approval is expected in early 2026.

Which standards should currently be used to prepare the statement?

Companies falling within the scope of the CSRD must prepare, tag and audit their sustainability statement in accordance with the requirements set out in the Directive and the ESRS.

Currently, the first version of the ESRS, published in 2023, is still in force.

In late 2025, EFRAG published drafts of the simplified ESRS and submitted them to the European Commission for review. The further process includes review and possible adjustments by the Comission, the development and approval of the delegated regulation, which, according to currently available information, is expected around mid-2026.

The European Parliament and the Council are then given time to examine the act and submit objections. If no objections are received within the specified period, the delegated regulation is published in the EU Official Journal and enters into force.

It is expected that the simplified ESRS will be applied from the FY2027 - with the possibility of using them earlier (for FY2026), depending on the date of entry into force of the delegated regulation.

What should companies do that fall outside the CSRD scope?

The narrowing of the CSRD scope will significantly increase the number of companies for which sustainability reporting will be voluntary. hese companies have a fairly wide range of options available, which can be grouped into two basic approaches: voluntary proactive reporting and voluntary reactive reporting.

Proactive voluntary reporting

Voluntary proactive reporting options exist through one of the voluntary frameworks or simplified ESRS.

Using one of the voluntary reporting frameworks:

- VSME - the European Commission-recommended standard for SMEs, which is also set as the cap for the amount and type of information that CSRD reporting entities can request from their partners outside the scope of the CSRD;

GRI - widely used global reporting guidelines that focus primarily on impact materiality;

- ISSB Standards that focus primarily on financial materiality;

Using the simplified ESRS:

as a guidance when preparing the company’s sustainability statement;

- or aiming to develop a statement fully compliant with the ESRS requirements;

Voluntary reactive reporting

Voluntary reactive reporting means that you choose not to produce a separate report, but instead provide ad hoc responses only to requests from customers, financiers, and other stakeholders.

If you do not know where to start your sustainability journey, contact us for an advice. Our team of experts can help with:

understanding and implementing ESRS and VSME;

assessing sustainability impacts, risks and opportunities;

mapping, development and improvement of sustainability data collection and the processes required for it;

XBRL markup of sustainability statements;

auditor’s assurance of sustainability reports.

Read more

All blog articles

ESG and sustainability

Amendments to the Law on Sustainability Disclosures regarding application dates have been adopted

· 2 min

Data analytics

Technology

Global business

XBRL

ESG and sustainability

ESEF

Driving smarter digital sustainability reporting: Orients Digit and Stratsys join forces

· 2 min